Executive Summary

Salazar Resources is an exploration company backed by a funded stake in a development project. The company aims to manage its treasury carefully and make a major discovery in Ecuador. Approximately 50% of the shares are held by management, friends and family and advisors with the remainder of the stock potentially held by stale bulls that have been in the company for years. Liquidity is poor, which is an ongoing problem that probably will not be resolved until Salazar is in a position to publish regular drill result news releases. Operating in Ecuador is very slow, but the government needs foreign exchange dollars so ultimately it is likely to be supportive of development.

The main asset in the portfolio, Salazar’s funded 25% in El Domo represents good value. El Domo is a high-grade VMS and it will be a mine. The entire rest of the portfolio can be considered true upside, ascribed zero value, and Salazar Resources trades at a discount. Fredy Salazar would appear to be the right man for Ecuador and he has built a good team around him, even though Salazar Resources, like most exploration companies tends to over-promise on its delivery timelines. A real plus-point for the company is its CSR work and corporate governance within the company is satisfactory.

Although funded for 2020, the Company will probably want to raise some capital for 2021 work. It is a bonus having income from advanced payments and management fees, which helps to reduce equity dilution. Regarding communication, Salazar is explaining its plans to the market in a coherent manner, which is a rarity among resource companies.

In short, Salazar Resources offers potenital of upside with the exploration derisked by the value of El Domo.

Introduction

Salazar Resources is a project generator exploration company operating in Ecuador. The company is headed by Fredy Salazar, the ex-head of exploration for Newmont Ecuador, and he has built up a exploration and CSR team around him. Salazar Resources has been listed on the TSXV since 2007 and it discovered and delineated the El Domo VMS deposit at Curipamba from 2008 onwards.

In 2017 the Curipamba project, with Indicated and Inferred resources at El Domo and a large untested exploration acreage, was farmed out to Adventus, a new special-purpose vehicle that was looking for zinc assets at the time. Salazar Resources is fully carried on a 25% stake in Curipamba all the way through to production. Salazar Resources also contributed two projects called Santiago and Pijili to an Exploration Alliance with Adventus. Both projects are at an early stage of exploration, and Salazar Resources is fully carried on a 20% stake in these two projects through to a construction decision. El Domo is at the Feasibility Stage of evaluation, with studies on 11Mt of 4.9% Cu equivalent material, and exploration within the broader Curipamba licence area ongoing. VMS deposits typically occur in clusters, and the NPV8 of the May 2019 PEA on El Domo alone was $288M. Exploration drilling at Santiago and Pijili will start once field is re-established after the coronavirus crisis is past. All work on Curipamba and El Domo, Santiago and Pijili is funded by Adventus. Salazar Resources receives a management fee of at least $350,000 per annum plus a $250,000 per annum advance royalty payment.

Salazar Resources also has its own portfolio of 100% owned projects. It has a wholly-owned exploration drilling subsidiary company called Andes Drill with three rigs that can generate income, plus three project areas in Ecuador:

- A. Ruminahui, a gold-copper porphyry target on trend with Llurimagua (CODELCO) and Cascabel (Solgold)

- B. Los Osos, a gold-copper porphyry target close to the 17Moz Cangrejos deposit (Lumina Gold)

- C. Macara, a VMS target potentially with a gold oxide cap, and nearby porphyry potential

The Company is focused on advancing its 100%-owned projects and then seeking partnership with mid-tier or major mining companies contingent on initial exploration results.

Strategy: What is the Company planning to do?

The plan, as laid out in the corporate presentation and reiterated in news releases from 1 March 2019 through to 14 January 2020 inclusive, is to work up the prospects, drill the best targets on a 100% funded basis, manage existing treasury and then farm out. Salazar wants to repeat the project generator blueprint established at Curipamba by targeting the next 100%-owned discovery and trading the non-core assets.

As an aside, all exploration companies want to make a good discovery, and all exploration geologists want to intersect a hundred metres or more grading one gram of material or more. Exploration is one of the few industries where real capital value can be generated overnight with the drill bit. Adam Smith, David Ricardo and Karl Marx, the early political scientists established Land, Labour, Entrepreneurship, and Capital as the essential Factors of Production, and a mineral discovery will result in the Land value changing dramatically. As it happens, for a discovery to be made, an exploration company needs to harness the other three Factors of Production, work, wit, and finance. Salazar has a stated ‘aim of making Ecuador’s next significant copper-gold discovery’. The entrepreneurship, labour and capital is in hand and what the shareholders want to see is the use of these three Factors of Production applied to the fertile geology of Ecuador, in the licenses carefully selected by Fredy and his team.

Returning to Salazar Resources’s strategy, in January it announced that the Company “plans to drill Rumiñahui, Los Osos and Macara on a 100% basis in 2020 and evaluate strategic options as the projects advance. The Company also awaits the re-opening of the national mining register later this year with interest. Salazar Resources has four project applications pending, and it is hoped that at least one of these new projects will be awarded when the register reopens. In addition the Company will submit several further applications for new projects and concession areas when the mining register opens.”

The Company then goes on to state that it, “intends to open formal discussion for farm-outs later in the year”. In parallel, work continues on the portfolio that has already been farmed out, where Salazar is fully carried by Adventus.

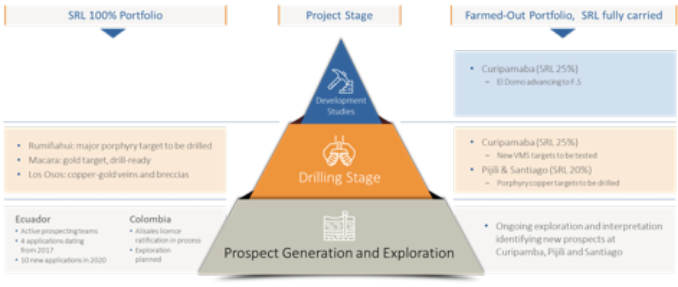

The graphic above is taken from the Salazar Resources website. The image shows the division between the self-funded projects (on the left-hand side)and the fully carried projects (on the right-hand side). Note that Salazar Resources references projects in Colombia, but little detail or information on these projects is given.

Capital Structure

Directors and management own approximately 30% of the issued shares, with Arlington Capital and associates in London, UK accountable for another 15-20% of the issued share capital.

Arlington Capital holds the warrants at C$0.12. Named institutional investors include US Global Investors, Merian Global Investors, Galileo Global Equity Advisors, Arlington Capital, and BlackRock Advisors. Salazar Resources listed in 2007 at C$2.00 per share, and current prices are C$0.16 per share.

Liquidity in Salazar Resources is poor, as can be seen from the wide spread (often 3-4c), the blocky share price chart, and the statistics which show average daily volumes of 26,000 shares per day.

After Salazar Resources signed the farm-out deal on Curipamba the share price held firm for most of 2017 and into 2018 before starting to decline from April 2018. Market conditions across the resources sector were weak in the second half of 2018. During 2019 the share price performed well, rising from a level of 11c at the start of the year to 20c by the end of that year. There were even two months in the 20-28c range before the virus hit. In the Covid-19 market correction in March 2019 the share price dipped to 12c before returning to around 20c.

Looking back at the longer history, the Salazar Resources initial public offering was C$10 million at C$2.00 per share in 2007. In the thirteen years since then it introduced new capital to the Company in 2009 (C$1 million), 2010 (two raises for a total of C$7 million), 2012 (C$3 million - Lundin lead order), 2013 (C$1.7 million - Trafigura lead order), and the last equity raise was in 2014 for C$1.1 million. In 2017 the Company completed royalty sales for a total of US$ 4.75 million.

Since the Adventus farm-out deals were signed in September 2017 Salazar has received US$600,000 annually via a mix of advanced royalties and minimum management fees. Warrants exercised in 2018 brought in C$1.5 million and in early 2019 the Company sold all of its Adventus shares for C$3.2 million. As at 30 September, 2019 the Company held C$4.27 million.

Not having issued equity since 2014 is a phenomenal achievement. Very few junior companies have managed to navigate the extremely difficult market conditions since 2012 with their share capital intact.

The sale of The Adventus shares in Q1 2019 is now looking like a very smart move.

Commodity

Governments around the world, and in particular the US government, have indicated that unprecedented fiscal and monetary stimulus will be deployed to alleviate the economic shock caused by the bid to control the Covid-19 virus. The quantitative easing, or helicopter money (call it what you will) devalues real assets and will push real interest rates deeply negative. This in turn will greatly enhance gold’s status as a real value, safe-haven asset.

In the short-term deceleration in economic growth will impact gold consumer demand and gold’s volatility may remain high, but in the medium to long term, the fundamentals of a sustained gold price rise are in place.

The principal commodities driving the economics of the Company are gold and copper. Underlying commodity price performance is not specific to Salazar Resources, and will be shared by all gold-copper focused companies.

Readers should note that there are fundamental differences between commodities. The prices of individual metals are essentially determined by the combination of current supply and demand, and expectations of future supply and demand. Information on supply (production and inventories) and demand (consumption) is not always readily available, nor accurate or transparent. Where information is scant or price-sensitive then prices can be blocky and extremely volatile. For the commodities that are widely studied and widely traded on terminal markets, such as copper and gold, their price movements are considered a barometer of general global economic health.

The choice of the commodity also affects how it is viewed by investors (whether at the equity level or at the project level). Individuals, analysts and financiers have a large pool of data on how to analyse gold or copper projects. Copper and Gold companies are relatively easy to understand, and therefore to value. The Resource types are well understood, the processing of gold is generally not too complicated or expensive, and the product can be sold at the mine gate into a highly efficient liquid market. The processing of copper is extremely well understood and although the projects come with high capital costs, there is a sufficiently large number of projects worldwide for analysts to be able to gauge and rank new exploration or development targets.

Thanks to its malleability and conductivity, Copper is central to modern living and the ongoing decarbonisation of energy supply and transport. The metal is key to the electrification of our economies as society grapples with climate change and a push to clean energy sources. In the short-term, copper demand will remain very weak due to the shock associated with the coronavirus economic shutdown.

On the supply side it is important to note the copper market has been in deficit for five years, drawing down inventories. It is likely that 2020 will be a net surplus year thanks to the demand shock, but supply will also be severely impacted by virus-related mine closures. Looking further out, ongoing supply deficits are widely anticipated. Chilean copper production (approximately ⅓ of global supply) remains constrained by low grades and scarcity of water. Elsewhere large-scale projects in workable countries are rare. In the medium to long-term we believe the copper supply and demand fundamentals remain intact, which should support its gradual price recovery.

Not only are the supply and demand fundamentals of each commodity different, but the relative difficulty of development also varies from commodity to commodity. For example, commodities with higher capital requirements, greater engineering and metallurgical complexity suitable only for major groups include platinum, rare earths, beneficiated iron ore (magnetite), hard-rock diamonds, low-grade nickel, low-grade copper, and coal. By the same token, commodities with more modest capital requirements, simpler engineering and metallurgical demands, suitable for mid-cap or more ambitious groups might include high grade copper or nickel, sulphide gold, high grade silver-copper-zinc.

Country

Ecuador is a traditionally socialist country that only recently placed mining at the heart of the economy. The country adopted the US dollar in 2000 and is therefore unable to undertake quantitative easing to pump-prime the economy which just leaves borrowing, inward investment or foreign export earning as potential sources of US dollars. Given the lack of other growth opportunities in Ecuador (oil, agriculture, tourism), the government reassessed its previously negative attitude towards mining in 2010 and adopted a committed mining policy. An ambitious new public mining plan is well underway, with a plan to increase exports to more than $2 billion by 2021 and for the mining sector to contribute as much as 4 percent to Ecuador’s GDP.

Two new, large-scale mines were commissioned in Ecuador in 2019, Fruta del Norte (gold) and Mirador (copper). Geologically the country has an abundant endowment, located as it is on a globally important mineral trend, the Andes. The country is relatively underexplored and with the revised State attitude to mining it has attracted a large number of international mining companies. Most of the major mining companies globally have an interest in Ecuador, presumably due to the mix of geological potential, limited exploration history, and the economic imperative to develop a mining industry being recognized by the government.

Considerable headwinds, however, remain. The international mining industry faces opposition from local environmentalists and indigenous communities, and a large proportion of the population has only had bad experiences of mining to date. There is a long tradition of environmentally damaging, unregulated, unsafe, non-tax-paying illegal mining in the country.

Another problem is that the government has struggled to manage the surge in interest in mining in Ecuador. Faced with the responsibility of making decisions that might have an impact on the Nation’s finances for generations to come, and with pressure accumulating from real and promised FDI, protest referenda, the arrival of most of the major mining companies, and by the general pace of events, the government effectively closed the Mining Cadastre in 2018.

The commitment to a modern mining industry is as strong as it has ever been, supported by public pronouncements, progressive changes to process and structure within the mining ministry, and of course, the stark reality of ongoing national budget deficits. But the government was faced with too many big decisions to be taken with insufficient internal expertise in too short a time-frame. The cadastre is still closed as the government is redesigning the mineral title permitting process to make the exploration expenditure more accountable, transparent and digital. No new licenses have been issued for 18 months and although in that time wrinkles in environmental permitting and water use permitting have been ironed out, there has been a knock-on delay in exploration activity. The Covid-19 crisis is only going to extend timelines.

Partnership Projects

El Domo, Curipamba

Salazar has a joint venture with Adventus on the Curipamba VMS discovery, whereby Adventus can earn 75% of the project by funding exploration and development expenditures of US$25M before October 2022. A feasibility study is expected to be completed during 2021, after which Adventus is required to fund 100% of the development and construction expenditures to commercial production.

Investment terms

Adventus Mining (“Adventus”) has the option to earn a 75% interest in the Curipamba Project by funding costs of US $25,000,000 (the “Earn- In”) over five years. Under the Curipamba Option Adventus has agreed to provide Salazar Resources with US $250,000 per year advance payments until achievement of commercial production, to a maximum of US $1,500,000. As operator, the Company also receives a 10% management fee on certain expenditures, with a prescribed minimum annual amount of US $350,000.

Adventus has notified the Company that it has incurred or funded costs totalling US$11,883,628 as at March 31, 2019 towards the Earn-In. Once the feasibility study is completed Adventus is required to fund 100% of the development and construction expenditures to commercial production.

Upon achievement of commercial production, Adventus will receive 95% of the dividends from the Curipamba Project until its aggregate investment, including the US $25,000,000, has been recouped minus the approximate Company carrying value of US $18,200,000 when the Curipamba Option was signed, after which dividends will be shared on a pro-rata basis according to their respective ownership. In certain circumstances where project development is delayed post earn-in, Adventus’ ownership position could be diluted.

PEA

A Preliminary Economic Assessment (“PEA”) for the El Domo volcanogenic massive sulphide deposit (“El Domo”), located within the Curipamba Project, Bolivar State, Ecuador was announced on 2 May 2019. Since then work on a feasibility study has continued. On 20 February 2020, updated metallurgical results were announced, showing material improvements over the PEA results from three composites collected and produced from the mixed, zinc, and copper geometallurgical zones, which enhance the economics of the project.

The El Domo resource at 4.9% copper equivalent is almost an order of magnitude higher than average global copper grades, which is reflected in the compelling set of economics, and the project is located in an increasingly pro-mining jurisdiction, with good infrastructure.

The PEA showed that El Domo can be a low-cost supplier of copper gold and zinc, generates cash flows after taxation of US$449M over the initial six years of production, and delivers an IRR of 40% with a payback of less than two years.

Geology and Mineral Resource Estimate

El Domo, located within the Curipamba project, Bolivar and Los Rios Provinces, Ecuador is, as noted above, a VMS deposit. VMS deposits often form in clusters, following the tectonic plate boundaries in areas of ancient underwater volcanic activity. The Curipamba VMS camp is one of three major hydrothermal centres in the Ecuadorian Andes, each separated by 50-60km. This is a typical distance between robust hydrothermal centres in ancient as well as modern systems. Each of these centres should contain a VMS compliment similar to that discovered in well-developed districts elsewhere, typically containing at least 20Mt, and possibly as much as 50Mt.

Sulphide mineralization at El Domo is principally located at the contact between a felsic volcanic dome and overlying volcaniclastic strata and is generally flat lying. It has been traced for approximately 800m in a N-S direction and between 350m and 500m E-W.

A Mineral Resource estimate for El Domo has been completed as part of the PEA to include all infill drilling completed in 2018. The updated, open pit constrained, Mineral Resource estimate for El Domo has an effective date of 2 May 2019 and is supported on information provided from 309 core boreholes, totalling 60,449 metres, completed between 2007 and 2018. The new Mineral Resource estimate has a total tonnage distribution of approximately 14%, 73%, and 13% classified in the Measured, Indicated and Inferred categories, respectively, as shown in the table below.

Total Mineral Resource for El Domo

Exploration Potential, Curipamba Project

The Curipamba project is comprised of seven concessions representing about 21,500 ha and includes the El Domo deposit. No systematic exploration work has been conducted on the greater Curipamba project area since the discovery of the El Domo deposit in 2008 by Salazar.

Looking at the wider potential of the area it should be noted that in well-developed VMS camps, each district is comprised of a cluster of deposits and each cluster is usually separated by 3km to 6km, a feature observed in the Curipamba area. Given the presence of multiple dacite domes, felsic and mafic subvolcanic intrusions, numerous “exhalite” type occurrences with distinctly anomalous gold, barite and zinc, and extensive hydrothermal alteration, the Curipamba district has all of the features of a major VMS camp, comparable in metal content to a classic camp such as in the Tasman Orogen or the Superior Province of Canada. El Domo may or may not prove to be the most significant deposit within the camp. Generally, well-developed camps typically contain a minimum of six deposits with economic metal content. One of these is normally the “giant”, containing more than 30Mt of ore. The potential for additional discovery in the Curipamba area is excellent as it is underrepresented in VMS compliment given its many positive geological attributes.

As part of the wider exploration effort on the Curipamba Project, a MobileMT geophysical survey was completed during 2019. The geophysical survey looks to have been designed for porphyry targets at Santiago, Pijili, and also lower priority for porphyries at Curipamba. It was announced in January 2020 that 15 exploration targets have been generated by the exploration team. The targets are classified as either volcanogenic massive sulphide (“VMS”)-related, such as the El Domo deposit, or porphyry-related. Planned drilling will test the higher priority targets in 2020, contingent on work being resumed after the virus-shutdown. A minimum drilling budget of 10,000m costing approximately US$5M (funded by Adventus Mining) has been approved for the evaluation of new priority targets areas and the continuing advancement of Curipamba-El Domo related studies.

Exploration Alliance, Ecuador

Salazar Resources has an Exploration Alliance with Adventus Mining that covers all of Ecuador. The Alliance ownership is 80% Adventus and 20% Salazar in an Ecuadorian Company, which will hold each exploration project up to a construction decision. Adventus is to fund all activities in the Alliance up to a construction decision on any project. Once a project reaches a construction decision, a separate joint-venture company will be formed for that individual project with pro-rata funding requirements, and be subject to a standard dilution formula. The Alliance is controlled by a steering committee consisting of two nominees from Adventus and one nominee from Salazar. A unanimous vote is required in specific business situations. Exploration activities of the Alliance are to be carried out by Salazar on a cost +10% basis under the supervision and approval of the Alliance Board. Salazar is required to bring all zinc-related (zinc as one of the top two metals) projects preferentially to the Alliance, but can also transfer non-zinc related projects into the Alliance upon agreement of the Parties.

Since the formation of the exploration alliance two projects, Santiago and Pijili have been introduced. Both are copper-gold porphyry exploration targets. See Figure 1 for project locations.

Santiago, Loja Province

The Santiago Project consists of a single concession that encompasses 2,350ha is located in a geological setting similar to the nearby Loma Larga deposit owned by INV Metals Inc.

Santiago is considered prospective for epithermal gold and silver and porphyry copper gold deposits. It features three large, surface geochemistry anomalies for gold, copper, and zinc. Numerous vein occurrences have been identified on the property thus far, which have yielded good chip sampling results for both gold and silver. They have also been previously subject to modest drilling campaigns by two operators on the property, including Newmont Mining Corporation that reported wide drill intercepts for copper-gold from surface down to 325m depth. These historic drill results cannot be verified, as the drill core is unavailable. An airborne geophysical survey (Mobile MagnetoTellurics, or “MMT”) was flown, generating a number of targets. Drilling is planned for 2020, contingent on being able to get back on the ground after the virus lockdown.

Santiago is subject to a 1.5% NSR that can be bought out for US $1,000,000 and a 4% net profits interest royalty that are held by INV Metals Inc.

Pijili, Azuay Province

Pijili is a 3,246 ha exploration licence (three concessions) within the Adventus-Salazar Exploration Alliance, approximately 150km from the major port city of Guayaquil. Mineral potential for Pijilí Project includes an untested epithermal gold-silver target, however, initial geological review is suggestive that there is a broader, larger scale porphyry target present. The Pijili project is adjacent to the Chaucha copper porphyry deposit originally discovered by a UNDP programme in 1964 and currently owned by Southern Copper.

Pijilí has never been explored with modern exploration techniques, such as geophysics, nor has there been any systematic geological mapping, geochemical sampling, trenching and/or drilling undertaken. Small-scale, legally permitted artisanal mining operations adjacent to the property are following precious metal-bearing structures via several small open pits and underground tunnels. There is secondary copper mineralization visible along the walls of the small open pits. Salazar staff have noted copper sulphide-bearing (chalcopyrite) veins in a valley bottom at the confluence of major creeks that also require additional follow-up. The MMT survey covered Pijili as well, generating a number of copper-porphyry targets. Drilling is planned for 2020, contingent on being able to get back on the ground after the virus lockdown.

100% Owned Portfolio, Ecuador

Salazar has three wholly owned projects in Ecuador. These are Rumiñahui, a copper-gold porphyry target in the north, Macara a VMS target in Loja Province, and Los Osos, a gold-copper porphyry target in El Oro Province.

Rumiñahui, Pichicha (Quito) Province

Rumiñahui (/’Roo-min-ya-we/) is a 2,910ha exploration licence (2 concessions) held 100% by Salazar Resources that hosts copper-gold porphyry targets. The licence is located approximately 100 km northwest and in the same province as Quito.

From a regional perspective Rumiñahui is part of the Imbaoeste District which, includes the (Eocene age) Alpala porphyry Cu-Au and (Miocene age) Llurimagua/Junín porphyry Cu-Mo deposits. These deposits are respectively associated with the Oligocene to early Miocene Saraguro Group and overlying similar Late Miocene to Recent arc sequences which are both developed and overlap throughout the belt, with the older succession predominating to the west.

Other deposits and occurrences are distributed along the Tertiary porphyry belt between these two districts, and to the north into Colombia and SE into Peru.

Rumiñahui can be considered a “grass roots” project stage of exploration having been subject to historic exploration by Newmont Ecuador in the 1990s and some exploration by Salazar Resources before the discovery of the El Domo VMS diverted funds and effort to the Curipamba project in 2008. The discovery of the Cascabel copper porphyry further established a porphyry trend, encompassing Rumiñahui, Llurimagua and projects in southern Colombia , even though Rumiñahui itself has not had much work done on it.

The prospect area is cut by the San Francisco river and exhibits a number of historic adits and old workings. Mapping and sampling have indicated the presence of gold-bearing, porphyry-style alteration and veining, shear zones, and quartz-veining. Sampling done by Salazar Resources geologists in 2006 confirmed gold mineralisation identified by Newmont Ecuador 1997. In-house sampling in 2006 indicated 2.76 g/t of gold over 55m; Newmont reported 3.8 g/t of gold over 50m at the San Francisco Prospect. Incidentally, the NI 43-101 technical report notes that Fredy Salazar was the geologist who sampled the prospect on behalf of Newmont Ecuador, which indicates that he has been exploring this prospect on and off for over twenty years. One obstacle is the volcanic ash that caps the hills and can be more than 5m thick, as discovered while trenching. The volcanic ash may mask the mineralisation and make soil geochemistry less effective than in other places.

From the limited work done to date the exploration model put forward in the Competent Person’s Report from 2007 was gold-silver in large quartz breccia/shear zones that can have multiple shears with semi-massive pyrite and chalcopyrite with gold, copper and silver. The main target was defined in 2007 as a large (>60m wide) shear/breccia zone with quartz breccia veins, semi-massive pyrite and chalcopyrite.

On 1 March 2019 Salazar Resources announced a strategic reset, in which it would be investing in the 100% owned properties for the first time in years. The company reported in July that in the first half of 2019 community liaison continued at Rumiñahui, supporting the Community Association with projects such as road repairs and agri-initiatives. A scout drilling plan and associated environmental impact assessment have been approved. The application for a water-use permit is underway. Salazar Resources has indicated that a Phase 1 drill programme of approximately 3,000m is planned for 2020 at Rumiñahui, contingent on the virus lockdown being lifted, and water permits being granted.

Macara, Loja Province

Macara is a 1,807 hectare exploration licence (2 concessions that are not contiguous) held 100% by Salazar Resources that hosts VMS targets in southern Ecuador. The licence has undergone mapping, soil geochemistry and rock-chip sampling.

The geology at Macara Mina consists largely of volcanic rocks of Cretaceous age. In Ecuador the sequences are known locally as the Celica formation whereas in the same basin over the border in Peru the same aged rocks are called the Lancones Formation. And the Lancones Basin hosts the Tambo Grande Cu-Zn-Au-Ag volcanogenic massive sulphide (VMS) deposits of northern Peru. Three unusually large VMS deposits occur within the vicinity of the town of Tambo Grande approximately 90km from Macara. The deposits are estimated to contain over 300Mt of material, comprising: TG1: 109Mt of sulphide ore grading 1.6% Cu, 1.0% Zn, 0.5g/t Au and 22g/t Ag plus 16.7Mt grading 3.5g/t Au and 64g/t Ag in oxide ore; TG3: 82Mt grading 1.0% Cu, 1.4% Zn, 0.8g/t Au and 25g/t Ag; and B5: resource not fully defined.

The reference to Tambo Grande is important because VMS deposits typically form in clusters, and the right conditions for mineral deposition can persist over long distances providing the geological setting is the same in both places. What Salazar Resources reports to be visible at Macara Mina is the same geological setting that is visible at Tambo Grande. And it should be remembered that the Tambo Grande VMS are some of the largest Cu-Zn-Au-Ag bearing massive sulphide deposits in the world. It should also be noted the deposits are relatively poorly studied and understood, but the key criteria that permitted such a phenomenal accumulation of sulphides may well persist across the basin. A PhD written on them in 2008 also notes that “the Tambo Grande deposits are particularly unusual amongst the ‘giant’ class of VMS deposits in that deposition largely occurred as seafloor-mound type…in seafloor depressions… [with] inherently confined hydrothermal venting”. The PhD goes on to relate that the main discoveries were guided by gravity geophysical surveys, echoing well-established exploration techniques that have been successful on VMS districts elsewhere in the world.

Salazar Resources mapping at Macara has identified a suite of basalts, andesites, and pillow lavas interpreted to be part of the same tholeiitic volcanic arc evident at Tambo Grande. Gold and base metal mineralisation is spatially related to a complex of hydrothermal breccias and stockworks in pillow lavas that are silicified to varying degrees and that occasionally host barite. Where the pillow lavas are brecciated the pillows contains <1% pyrite, chalcopyrite and bornite with occasional sphalerite in the matrix, and there is less intense mineralization in the pillows themselves. Where the stockworks contain barite veinlets and exhibit more intense silicification, often characterized by iron oxide staining, the gold and silver grades are elevated. The Company has reported 9.94g/t gold in soil samples, and 29.60g/t gold in rock samples from Macara, which are extremely high-grade results. Drill targets are under evaluation.

Los Osos, El Oro (Gold) Province

Los Osos is a 229ha, single concession, exploration licence located in the Cerro Pelado-Cangrejos mineral district within El Oro Province (Gold State) in southwest Ecuador.

The licence is held 100% by Salazar Resources and hosts a system of veins rich in gold and silver, combined with hydrothermal breccias and mineralised gold-copper porphyries. Several quartz-tourmaline breccias mineralised with chalcopyrite and pyrrhotite present on the property.

Artisanal miners have historically worked some of the veins, and small scale mining has been active on Los Osos and the adjacent properties for over 15 years. In a news release from January 2020, Fredy Salazar said that “what makes the Osos project so compelling is that it is only 10 km south ofthe 17 Moz Cangrejos gold project and Pacho Soria, our Chief Geologist, led the discovery team at Cangrejos. He knows the geology at Cangrejos intimately, and recognizes a very similar mineralizing system at Los Osos. Extensive artisanal work at Los Osos historically focused on high-grade, narrow veins. The potentially higher tonnage bodies with disseminated mineralization will be drill-tested for the first time by Salazar Resources.”

Salazar Resources also reported that mineralization is present in multiphase hydrothermal breccias, stockwork zones, and porphyry intrusions. Furthermore, when present, the mineralization in the rocks is pervasive and widespread, consisting of pyrite and chalcopyrite in varying quantities, with an apparent correlation between the intensity of sulphide mineralization and gold and copper grades.

The main exploration target for Salazar Resources are the potentially large-tonnage porphyry-related hydrothermal breccias, and to date multiple breccia bodies have been identified within the concession area, some up to 300m by 200m in size. Salazar Resources is currently evaluating drill targets on the property.

Drill Rigs: Perforaciones Andesdrill S.A.

Salazar Resources has a wholly-owned stand-alone subsidiary, Perforaciones Andesdrill S.A that owns three diamond drill rigs. The rigs provide drilling capabilities for Salazar Resources or its ventures with Adventus. In addition, the rigs can service third parties when available and are a potential source of income for the Company. Salazar Resources drilled approximately 70,000m at El Domo using its own rigs.

The benefits of owning drill rigs is tenuous. Although fees can be earned, the Company has to carry stand-by costs. Also, Salazar Resources’ expertise is finding new deposits and managing community relations in Ecuador, not running the logistics of a drilling Company.

The rigs may be useful for early-stage or Phase 1 or 2 drill programmes. Once a discovery is made, full drill-outs are best done using dedicated drilling contractors.

Management is Key

Board of Directors

The Board of Salazar Resources appears to functioning adequately. Immediate observations are that it is too big for a Company of this size. Five directors is probably enough at this stage of Company development.

A second observation is that there are no real mining non-executives directors in the Company, nor a chairman. Crux Investor likes to have a chairman there to ask difficult questions of the CEO. Crux Investor also likes to see independent non-executive directors with relevant experience to keep the executive team on their toes.

Fredy Salazar, President & CEO

Salazar is a professional geologist registered in Ecuador and he holds a bachelor’s degree in geology and a master’s degree in environmental sciences from Central University, Quito. For a time he was Newmont’s regional exploration geologist, reviewing and evaluating over 100 gold prospect submittals and he has an extensive and detailed knowledge of Ecuador’s geological potential. Salazar also formed and ran one of Ecuador’s most important Environmental Consulting firms in a mineral downturn. In 2004, Salazar resumed resource exploration and in 2007 he founded Salazar Resources Limited and listed the Company on the TSX Venture Exchange. Fredy is well known and well respected in the mineral industry and within government circles in Ecuador.

Merlin Marr-Johnson, Executive Vice President, Corporate Secretary

Marr-Johnson is a graduate in geology from Manchester University and holds a Master’s Degree in Mineral Deposit Evaluation from the Royal School of Mines, Imperial College. He has 25 years’ experience in the minerals sector, including work as an exploration geologist for Rio Tinto, an analyst for HSBC and a portfolio manager for Blakeney Management.

Marr-Johnson has worked on projects in South America, Africa, Central Asia and Europe, and as CEO he has brought two companies to AiM, London. He speaks several languages, including Spanish.

Nick DeMare, Director

DeMare is a chartered accountant and has been a director and officer of many publicly listed companies in Canada since 1986. Nick earned his bachelor of commerce from the University of British Columbia in May, 1977. Since 1991, as president of Chase Management Ltd., he has specialized in providing accounting, management, securities regulatory compliance and corporate secretarial services to companies listed on the TSX-V and its predecessors. DeMare is currently a director and/or officer of several TSX-V-listed companies.

Etienne Walter, Director

Walter is the honorary consul general of the Republic of Ecuador, with jurisdiction over the provinces of Alberta and British Columbia, the Northwest Territories and the Yukon Territory. His appointment was in December, 1993, with recognition by the Canadian government since March 17, 1994. He earned his diploma in hotel management and financial administration from the Ecole Hotelier de la Societe Suisse des Hoteliers in Lausanne, Switzerland, in November, 1972. Since coming to Canada in 1975, Walter worked for public and private corporations until forming his own company, Andes Trade and Investment Ltd.

Jennifer Wu, Director

Wu has 20-years diverse experience in metals and mining financing, risk management, and business planning and development. She has a B.S.in information management from Renmin University of China and a M.B.A. from Wake Forest University.

She holds the Certified Financial Analyst (CFA) designation. During an 11-year career at JP Morgan Chase and Citigroup, she rose to Senior Vice President in risk management. Since 2011, she has specialized in metals and mining investments by Chinese private and state-owned-enterprises and investment funds.

Pablo Acosta, Director, CFO

Acosta is an Ecuadorian certified public accountant and has been a director and officer of several private companies in Ecuador since 1985. He earned his bachelor of commerce from the Pontificia Universidad Catelica del Ecuador (PUCE), Quito Ecuador, 1987; audit manager at Romero & Asociados from 1985 to 1987; managed Bermudez & Asociados Cia. Ltda. audit department from 1987 to 2003. Acosta has specialized in providing accounting, external auditing, project and operations auditing, instructors training, company valuations, finance management, cost and budget planning, quality management standards, and environmental matters. Since 2003, He has worked with Salazar since 2003.

Senior Management and Advisors

Freddy D. Salazar, Manager, Corporate Development

Freddy David Salazar holds a BA (hons) in Global Financial Management from Regent’s Business School, London and Ecuadorian certifications in Tax. Salazar Jr joined the Company in 2010 and since 2014 has overseen transactions and new business for Salazar Resources. He is completing an MA in Tax at Universidad Andina Simon Bolivar, Quito.

Arlington Group, Financial Advisor

In January 2019, Arlington Group out of London, UK was retained as the Company’s exclusive capital finder and financial adviser for a term of 24-months. Arlington has commodity sector expertise, and works closely with management teams in turnarounds, refinancing, and restructuring mandates. Arlington has originated, sold and distributed over $3 billion of natural resource deals to date.

Timelines: Plans, Delivery, Reality

The rate of exploration for all companies operating in Ecuador has been slow since 2018 for a number of reasons, that includes:

- Covid-19 and the (hopefully temporary) delays to the work cycle.

- Social licence to operate, or lack thereof, largely determined by the quality of community relations.

- Hold-ups across governmental departments, largely caused by a lack of coordinated political will and insufficient institutional capacity.

- The internal organisation of individual companies, and the ability to meets their own delivery plans.

For Salazar Resources, the Covid-19 enforced shutdown means that environmental baseline and hydrogeological studies at Curipamba have been suspended along with all site work. Accordingly, the delivery of the feasibility (due 5 October 2021 is likely to be delayed by the number of days that site activities are shut down for starting from March 17, 2020. On other projects, fieldwork has been curtailed.

The social licence to operate in Ecuador is absolutely vital, and can cause significant delays when the local community turns against the project. CSR is an area where Salazar Resources excels (more will be discussed in the ESG section below). Salazar Resources is an Ecuadorian company, and Fredy Salazar has a genuine desire to advance the economic development of Ecuador through its natural resources, which means that the Company has real social capital to enable it to progress at the ground level in a meaningful way. Community Relations and Sustainability are so often considered soft issues, but getting it wrong can cause real shareholder value destruction.

Perhaps the greatest cause of delayed progress in Ecuador in recent years is the government itself. Despite a pressing need to establish a broad-based mining industry to generate foreign exchange earnings and direct and indirect jobs, getting a smooth process established is proving difficult. For several years the anti-mining lobby has made Environmental Permits hard to grant, until the Environmental Ministry was brought under the wing of the Ministry for Non-renewable resources. Since late 2018 environmental permits for exploration have been easier to realise. Similarly, the lack of Water Permits has held up a significant amount of drill programmes since 2018. In late 2019 the government replaced the head of the Water Board and brought the Water Board under the remit of the Ministry for Non-renewable resources. Finally, the heads of the key departments need to sign-off on an exploration programme are all within one Ministry. Hopefully this will lead to more timely processing of permits to allow drilling. It is worth noting that exploration drilling recently resumed at Curipamba, but that water permits are still awaited for projects within the 100% Salazar Resources portfolio.

A further delay lies with the Mines Department of the Government which has not issued any new licenses since 2018, as the mining cadastre is being revamped. Overwhelmed by a flood of real and promised exploration dollars, the government stopped issuing exploration permits from the Mining Cadastre in 2018. The latest government projections are for the cadastre to start issuing licenses in Q3 2020, although with the coronavirus adding to delays, a more realistic assessment is Q4 2020. The revamped Mining Cadastre will result in a redesigned mineral title permitting process to make the exploration expenditure more accountable, transparent and digital. No new licenses have been issued for eighteen months.

In the face of all these issues it is unsurprising that Salazar Resources has struggled with delivery timelines in the past couple of years. In Q1 2019 the Company indicated that it would drill Rumanhui and Macara during 2019, and then in Q1 2020 it gave a new timeline for drilling the same properties during 2020.

Looking ahead, the corporate presentation notes that Salazar Resources has a funded US $2.6m budget for 2020 that incorporates the option to drill up to 8,500m on its 100% owned portfolio. As at September 30, 2019, Salazar Resources had C$4.27m in cash and the Company also receives income in the form of advance payments and management fees from its funded joint ventures. The guaranteed income from Curipamba is a minimum of US$600,000 per annum and Salazar Resources will earn additional management fees for exploration services provided to the Exploration Alliance for work on Pijili and Santiago. Salazar Resources can generate further income from its wholly-owned subsidiary, Perforaciones Andesdrill S.A that owns three diamond drill rigs.

Exploration companies are always need to strike a balance between preserving treasury and creating value by ‘making discoveries’. In terms of the metrics that investors can see and understand, this typically means mineralised drill intersections. Maps, and prospects, and samples are all useful indicators in the journey towards a discovery, but in order to get the share price moving mineralised drill core is the key ingredient.

Given the headwinds of Covid-19, and lack of water permits it would be a miracle for Salazar Resources actually to be able to drill 8,500m and spend US$2.6M in exploration this year. With fewer opportunities to spend value-accretive money in the ground it will be important for the Company to take steps to maintain treasury during a year where exploration activity is reduced. The traditional way to do this is to reduce headcount, avoid spending on non-core activities and reduce salaries. It should be noted, however, that Salazar Resources has good form in preserving treasury, and that some of the corporate overhead is actually covered by the farm-out deals with Adventus Mining. As a case in point, although 2019 was not a particularly busy year in terms of exploration results and no drilling took place, Salazar Resources started the year with C$2.8M, and at the start of October in the same year, the Company had C$4.3M.

ESG – three small letters that cover a huge range of topics

ESG encompasses a broad range of topics, under its three headings of Environment, Social and Governance. The environment is all about climate change, biodiversity, waste, water and resource use, pollution. The ‘social’ part of the acronym covers human rights, labour practices, safety, health, community, and diversity. And the last word ‘Governance’ includes corporate governance, ethics, compliance, executive pay, diversity, and lobbying within its remit.

Historically ESG has been viewed as a soft (and therefore not particularly important) issue. Nowadays, however, ESG is a hot topic. Tell Vale, with their tailings dams disasters, or Teck dropping its tar sands projects that the environment doesn’t matter. Try telling investors that the company is not prioritising its local biodiversity and water supplies. In a hyper-connected world where every cell phone has a camera and internet access a company’s environmental record is always under scrutiny, especially by local communities. Damage the environment and you risk losing social licence to operate. And companies that cannot access their mine sites because of a loss of trust with local communities can see major value destruction through time delays and falls in share price.

Today there is a combination of societal pressure from stakeholders such as local communities as well as investors and there is regulatory pressure both at a national and international level. Increasingly ESG ‘credentials’ are needed for debt and equity financing from large institutions. Good ESG procedures and standards help companies stand out from peers by being able to work when others cannot due to good social capital, or a strong licence to operate. Another reason is that there is a growing pool of capital available for leading-ESG compliant companies.

Salazar Resources is a small company so the ESG measures it takes should be commensurate with its size. Equally, it should have a good set of policies in place so it has the capacity to grow if need be.

From an environmental and social perspective, Salazar Resources appears to be operating well. The flavour of the corporate video captures integration with the local community and the local environment. Compared to other corporate videos, it feels more personal, and the enthusiasm of the team for the community and the football team is palpable, and the closing line is ‘We are Ecuadorian’.

In terms of corporate governance, it is interesting to see that Merian Global Investors has taken a stock position in Salazar Resources, through the gold fund. Merian have a stringent approach to responsible investing and stewardship, and it is a stamp of ESG approval as much as investment case to have them on the share register.

Looking at the make-up of Boards in general, Crux prefers to see a non-executive Chairman or strong independent directors looking after the strategic interests of all shareholders, and providing oversight of the CEO’s overall strategy and delivery. A well-run company will ensure that operational progress is made, that the award of any contract or remuneration package is in line with best practice, and critically that communication with the market is done in an appropriate manner with website, news releases and presentations are kept up to date and proportional in tone (neither too promotional nor lacking in enthusiasm). The majority of the input, and the energy required to run the company and address all of these issues does, of course, come from the executive team. The non-executive directors really come into their own when the executive team is not performing well. At present Salazar Resources is doing ok, with the appointments of Merlin Marr- Johnson and Arlington Group last year filling a capital markets and communication gap that had existed. Still, as the Company is looking to grow in the coming years it needs to continue to ensure that the appropriate corporate governance standards are maintained.

When will the Company need to raise money again?

Before centering in on Salazar Resources, it might be worthwhile to look at how exploration companies spend money, and why investors should care about exploration companies at all.

Mineral deposits, truly economic mineral deposits are very hard to find but is difficult to know right at the start which prospects are going to make it all of the way to the pinnacle (being a mine) and which prospects will fall off the ziggurat (subeconomic rock that is never going to come out of the ground). From geological concept, through to target, prospect, drill target, drill results, phase 2 drilling and onwards, some prospects will start accruing value, others will not. Good management teams have the discipline to drop projects when it becomes apparent that they will not make it.

All exploration work needs funding, and the more advanced the project is, the more it is technically derisked and the more the next stage of work costs. Investors are typically attracted to exploration companies because of the potential for spectacular returns (striking it rich), even though the risk associated with early stage projects is high. Because the technical risk of making a discovery (or not) is so high, investors need to be comfortable with a raft of other factors before embarking on funding the next round of work or not. A quick checklist would include the headings of this report so far: Capital Structure, Strategy, Commodity, Country, Projects, Management, Timelines and ESG. Having satisfied oneself that all of the above is in order, the next question is what will the Company do with the money?

The theory behind exploration is that a company invests $1 in the ground and turns it into $5 or $10 worth of ‘exploration value’ making a discovery. If it does that, then investors will fund the next round of work. Trubliz, it is hard to find economic mineralisation in drill core, it is hard to make that breakthrough discovery.

Here are some of the things that investors often forget.

- The G&A cost of running a small company is a large percentage of the money outflow. This means that in the example used above the $1 invested actually represents, say, 40 cents in G&A (more in bad companies) and only 60 cents in exploration

- Companies explore several prospects at the same time. This means that in the example used above (60 cents going into exploration), there may be only 20 cents going into each of three projects, or 12 cents going into each of five projects. For one of the projects to generate value at the Company level, a small amount of money needs to go a long way.

- Problems arise when a small company carries out a slow drilling campaign, which is a toxic mix of high spend with no result. Having the exploration camp geared up for drilling, incurs a significant daily cost so any delay to the programme or just having a slow drilling rate can chew up budgets. It is much better if exploration companies do all of the lower cost work first (such as mapping, geochemistry and geophysics) before hitting the drilling campaign hard and fast.

In short, exploration companies carry high investment risk, including high technical risk as well as offering the promise of high reward on discovery. Investors should make sure that the Company has done everything in its power to derisk as many aspects as possible of its investment thesis.

It is also equally true that Company management needs to have confidence in getting exploration work done. Shareholders do not want to see any level of inactivity, as this just means that G&A is spent while no technical progress is made. Management needs to strain every sinew to ensure that exploration results are delivered. As long as economic mineralisation is being discovered the capital markets will fund the next round of work.

Turning now to Salazar Resources, the company presentation shows a waterfall chart of funds for 2020. Starting with US$3.5M in treasury, plus the US$600,000 management fee, Salazar has US$4.1M in the kitty. With exploration work including drilling, G&A, and licence fees to pay the Company expects to spend US$2.6M over the year, leaving US$1.5M in treasury by year end, but with work on the licenses having advanced. As discussed, the ideal would be that the US$2.6M investment is turned into something greater, say, US$10M or more, of capital value. At that point more equity can be raised, and or a farm-out deal can be entered into. As was noted in an earlier chapter getting a farm-out deal completed by Year End is a tall order, so it is likely that Salazar Resources will want to do a treasury top-up at some stage around the year end.

It is important for companies to raise money before they really need it, to maintain a treasury buffer and to prevent the share price being squeezed lower. As an absolute minimum, companies should not let treasury fall below US$1M, and as a rule of thumb anything less than US$1.5M should be avoided. When it comes to capital raises, it makes sense to enable two years of proper exploration work to be carried out, so a company like Salazar Resources would probably benefit from having US$3-4M in treasury after the next capital raise (remember that it generates at least US$600,000 per annum from advanced payments and management fees, and that the drill rigs may contribute some income).

How does the Company communicate with investors?

The way in which exploration companies engage with the market and present its information is a vitally important aspect of the business. In the modern day and age it is crucial to have an up-to-date website, a clear investment thesis, at least one presentation that addresses the overall investment case for the Company (even if there are other presentations that address technical aspects of the Company in greater depth), and regular activity-based news releases.

Looking at the Salazar Resources 2020 news releases, there are 6 so far in the year. Pleasingly these are almost all activity-focused, and note that the ratio is 2:1 joint with Adventus versus on the 100% Salazar portfolio. This 2:1 ratio is more or less proportionate to investment spend. Salazar has 3 projects with Adventus and 3 that are wholly owned, and Adventus plans to invest over US$5M in Ecuador this year and Salazar plans to invest US$2.6M in 2020.

- Mar 18, 2020: Adventus and Salazar Place Ecuadorian Project Site Activities on Hold As a Result of Government’s COVID-19 Public Health Decree

- Mar 5, 2020: Adventus and Salazar Secure Key Lands for El Domo Development and Announce Ramp-up of Drilling With Three Rigs at Curipamba

- Feb 20, 2020: Adventus and Salazar Provide Positive Update of Metallurgical Results for El Domo Deposit, Curipamba Project

- Jan 29, 2020: Salazar Provides Updates on Exploration at Los Osos and an Executive Appointment

- Jan 21, 2020: Adventus And Salazar Announce 2020 Ecuadorian Exploration Plans And Drill Rig Mobilization

- Jan 14, 2020: Salazar Provides a Corporate Update On Its Wholly- Owned Portfolio

The emergence of news releases from Salazar Resources independent of Adventus Mining is a relatively new development. Once the farm-out agreements were signed in September 2017 Salazar Resources appears to have left formal communication with the market to Adventus Mining. From September 2017 to January 2019, Salazar Resources published one news release regarding its wholly owned portfolio (January 2018, the acquisition of the Macara licenses) and eleven news releases that were written by Adventus Mining and published jointly. Things changed with the appointment of Marr-Johnson to the Board, and Arlington Group as financial advisor on 25 January 2019, with the strategic reset of the company announced to the market on 1 March 2019.

The Salazar Resources presentation and website are relatively clear and up to date. The investment case and business strategy are laid out in the presentation, which is welcomed.

Red Flags

- Lack of liquidity in the stock.

- Slow permitting (water, environmental).

- Mining Cadastre not issuing licenses since 2018, and delayed again to Q3 2020.

- Anti-mining protests in Ecuador – vocal and populist.

- Cumbersome Board, too big for an exploration Company.

- Salazar has been slow to deliver on exploration in past 18 months, perhaps due to Ecuador-wide permitting issues.

Green Lights

- El Domo, fully carried 25% stake all the way to production.

- Santiago, Pijili, fully carried 20% stake all the way to construction decision.

- $600k annual income, minimum (from farm-out deal).

- Project generator, equity dilution protection model.

- No equity issue since 2014.

- Sale of Adventus Mining equity in Q1 2019. Excellent move in hindsight.

- Exposure to gold and copper.

- Focus on exploration – sticking to what they are good at doing.

- Mining companies focusing on Ecuador. Peer group validation.

- Ecuador needs a responsiblemining industry built as soon as possible.

- El Domo PEA showed strong economics. It will be a mine.

- ~$70M attributable value for Salazar Resources.

- Likely to be more VMS deposits at the Curipamba Project.

- Pijili and Santiago host known mineralisation, so relatively low-risk exploration.

- Rumiñahui (100% SRL) on trend from major porphyries, good gold potential.

- Macara (100% SRL) excellent VMS and gold oxide exploration targets

- Salazar Team has a proven track record of discovery and best placed to make the next discovery in Ecuador.

- Salazar and Marr-Johnson a trustworthy team.

- Best in class CSR.

- Well-funded relative to most small explorers, with C$4.3M Sept 30, 2019.

- Good communication with stakeholders.

- Competitive valuation, trading at a significant discount to NAV, and ignoring all of the exploration potential for the Company which is the main reason for owning stock.

Valuation

Investors in exploration companies need to understand what is the value of the investment proposition in front of them? Assuming that an investor is keen to take the risk/reward profile that an exploration company carries, the next task is to understand the building blocks of value for the company in question. Breaking the analysis down into bite-sized chunks is often a useful approach. Once the various value (or liability) components are understood then they can be added back together again to arrive at a Net Asset Value, or NAV. Typically, the equation runs like this:

NAV = cash (or cash equivalents) + value of main property + value of secondary projects (if there are any) + embedded option value

The term ‘embedded option value’ is a catch-all phrase which covers commodity and country potential, and the ability of management to find new licenses, make deals, and generate value by turning exploration dollars into exploration results. Once the NAV number has been calculated, it is then time to compare the NAV with what value the market is ascribing to the Company in the form of its market capitalisation (number of shares in issue × share price). If you divided the market capitalisation figure by the NAV figure one arrives at a P/ NAV or price to NAV. If the P/NAV is greater than 1, the market is paying more than full value for the company, which is usually a sign that investors believe that there is a strong case for the NAV to grow in the future. If the P/NAV is less than one, the market is ascribing a discount to the value of the company, which is usually a sign that investors believe there are significant risks surrounding the business plan.

At this point, it is worth scanning the horizon and have a quick look at what the P/NAV is for other companies offering a similar investment thesis, or that can be considered peers. If the Company an investor is looking to buy is trading at a higher P/NAV multiple than its peers it can mean that there are better value choices out there. Equally it could mean that the company in question offers greater scope for success. There is no simple answer, but the more one understands about the investment landscape, the greater the chances are that the investment one makes will be a good one.

Turning to the NAV calculation for Salazar Resources (SRL), the calculation will be as follows:

NAVSRL= cash SRL + value of main project SRL + secondary projects SRL + embedded option value SRL

Cash SRL = C$4.3M or US$3.5M as of end September, probably closer to US$2.5M now(being conservative)

Value of main project SRL = value of 25% stake in El Domo, which from the PEA the NPV was $288M × 0.25 = $72M. This figure can be used because Salazar Resources is fully carried all the way through to production and will not have to dilute further to reach this milestone.

Embedded option value SRL = the 100% wholly owned portfolio, plus the carried interest in Pijili and Santiago. Hard to say, pick a number, how about US$5 million?

Therefore

NAVSRL = 2.5 + 72 + 5 = 80, US$80M

Compare this figure with the market capitalisation of (122 million shares × 20c, or 15c US = 18.3) US$18.3 million.

On this basis Salazar Resources is trading at 0.18x NAV. Even if one ignores the value of the exploration projects, so the NAV is only $75m, the company is still trading on 0.24x NAV. Rounding to the nearest decimal place, it would be fair to say that Salazar Resources is trading at around 0.2x NAV.

Another way of looking at Salazar Resources is that the value of its stake in El Domo, Curipamba, is much larger than the market capitalisation of the company, so everything else in the Company is in for ‘free’. The next set of questions it leads to are all about the reliability in the value of El Domo.

Will it actually be a mine? Yes, this VMS is big enough, rich enough, and important enough for Ecuador that it is safe to say that it will be a mine.

Do the rises in the gold price offset the falls in the copper price when it comes to valuing the project? The base case for the NPV was carried out at $3.15/lb copper, and $1,350/oz gold. Spot prices are down 26% for copper and up 25% for gold from the base case figures, so the base case is probably still an appropriate number to use given that the revenue splits are relatively even between copper and gold.

What are the timeline risks associated with the development of El Domo? Everyone is watching the development of Covid-19 and there is, of course, risk of delay associated with the virus. In the most recent presentation by the government of Ecuador in mid-April, a slide was published showing that production at El Domo, Curipamba is expected in 2024

Does Salazar have a funding risk or need to raise capital to see El Domo become a mine? Because Salazar Resources is fully carried all the way through to production, Salazar does not have to raise money or issue equity to see El Domo reach production. The company, through the deal structure established in 2017 is funded for its share of the capex, and all other aspects of the work within the project area.

The P/NAV multiple for Salazar Resources (0.2x) shows that El Domo needs to be discounted down to a very small number before any value is attributed to the rest of the Salazar Resources, which comes down to the exploration portfolio of the other five licenses and the ability of Salazar Resources to generate new discoveries in Ecuador.

Conclusion: What does this all mean?

Making an investment decision in any company requires the investor to be comfortable with the level of risk one is being exposed to, relative to the potential rewards that the investment offers. Buying a share at a price of, say, 20 cents, investors need to be comfortable firstly that the 20 cents won’t shrink to 10 cents or less, and that it has a good chance of rising to 40 cents, or more.

Classical economic theory with its roots in the Enlightment of the 18th Century notes that the Factors of Production include Labour, Entrepreneurship, Capital, and Land. Each of these four factors (Board and Management, Strategy, Treasury and access to Capital, plus Projects and Exploration Licenses – when translated into modern parlance) are needed to make an exploration company successful. This report hopefully shows that Salazar Resources is well-equipped with geologists, strategy and funds to apply these three Factors towards the Land (Salazar licenses) of Ecuador, and continue to create value both at El Domo, and with discovery elsewhere in the portfolio. Real value can be generated through the drill bit by exploration success.

Salazar Resources is trading at a discount to the fair value (0.2x PNAV) of its stake in El Domo, so it could be argued that inves¬tors effectively have a free option on Fredy Salazar and his team making another discovery in Ecuador. If you are looking for an exploration company through which to gain exposure to the gold and copper cycles, potentially Salazar Resources is an ‘equity di¬lution-protected’ company offering a good value entry-point and a good chance of making another discovery.

Ecuador is a country that cannot afford to do anything other than support its mineral industry and speed up permitting. It is also an incredibly mineral-rich country that has not been subject to intensive systematic exploration. As slow as it may be currently to get permits processed, the mining industry has woken up to the fact that if you want to increase your chances of finding the next generation large and rich copper or gold deposit that is at surface, Ecuador seems the place to be. Every major company is hunting for ground, and Salazar Resources has home advantage.

Warren Buffet recommends buying shares in good businesses, shares that you would be willing to hold for ten or twenty years. The company manages its treasury well, and it has structured great farm-out deals that will continue to accrue value as El Domo moves towards production. Salazar has annual income from management fees, advance royalties and potentially the drilling company. The Company has built up a portfolio of highly prospective assets that it will be drilling soon. Fredy Salazar and his team are Ecuadorian, have been working and making discoveries for 20-years in Ecuador. They have the in-house ability to find the next big discovery and nurture it to production.

It is the kind of company that you should have in your portfolio now, and you will probably still want it in your portfolio in ten years’ time.

Appendix – Brief Summary

A very brief summary of Salazar Resources could be presented in two tables, the first asking the Key Questions and the second providing Summary Answers. Something like this:

These CRUX Reports are written for expert investors AND for people new to natural resource investing. But whether you are an expert or a newbie, we all have the same driver. We invest to make money. Sometimes investors get emotional about the investment. They actually think they own a mine. They don’t. They own shares in a company. So focus on your investment strategy, work out the best plan for your needs, stick to the fundamentals and remember that the only way you make money is if your shares go up in value… assuming you don’t forget to cash them in!

Executive Summary

Salazar Resources is an exploration company backed by a funded stake in a development project. The company aims to manage its treasury carefully and make a major discovery in Ecuador. Approximately 50% of the shares are held by management, friends and family and advisors with the remainder of the stock potentially held by stale bulls that have been in the company for years. Liquidity is poor, which is an ongoing problem that probably will not be resolved until Salazar is in a position to publish regular drill result news releases. Operating in Ecuador is very slow, but the government needs foreign exchange dollars so ultimately it is likely to be supportive of development.

The main asset in the portfolio, Salazar’s funded 25% in El Domo represents good value. El Domo is a high-grade VMS and it will be a mine. The entire rest of the portfolio can be considered true upside, ascribed zero value, and Salazar Resources trades at a discount. Fredy Salazar would appear to be the right man for Ecuador and he has built a good team around him, even though Salazar Resources, like most exploration companies tends to over-promise on its delivery timelines. A real plus-point for the company is its CSR work and corporate governance within the company is satisfactory.

Although funded for 2020, the Company will probably want to raise some capital for 2021 work. It is a bonus having income from advanced payments and management fees, which helps to reduce equity dilution. Regarding communication, Salazar is explaining its plans to the market in a coherent manner, which is a rarity among resource companies.

In short, Salazar Resources offers potenital of upside with the exploration derisked by the value of El Domo.

Introduction

Salazar Resources is a project generator exploration company operating in Ecuador. The company is headed by Fredy Salazar, the ex-head of exploration for Newmont Ecuador, and he has built up a exploration and CSR team around him. Salazar Resources has been listed on the TSXV since 2007 and it discovered and delineated the El Domo VMS deposit at Curipamba from 2008 onwards.

In 2017 the Curipamba project, with Indicated and Inferred resources at El Domo and a large untested exploration acreage, was farmed out to Adventus, a new special-purpose vehicle that was looking for zinc assets at the time. Salazar Resources is fully carried on a 25% stake in Curipamba all the way through to production. Salazar Resources also contributed two projects called Santiago and Pijili to an Exploration Alliance with Adventus. Both projects are at an early stage of exploration, and Salazar Resources is fully carried on a 20% stake in these two projects through to a construction decision. El Domo is at the Feasibility Stage of evaluation, with studies on 11Mt of 4.9% Cu equivalent material, and exploration within the broader Curipamba licence area ongoing. VMS deposits typically occur in clusters, and the NPV8 of the May 2019 PEA on El Domo alone was $288M. Exploration drilling at Santiago and Pijili will start once field is re-established after the coronavirus crisis is past. All work on Curipamba and El Domo, Santiago and Pijili is funded by Adventus. Salazar Resources receives a management fee of at least $350,000 per annum plus a $250,000 per annum advance royalty payment.

Salazar Resources also has its own portfolio of 100% owned projects. It has a wholly-owned exploration drilling subsidiary company called Andes Drill with three rigs that can generate income, plus three project areas in Ecuador:

- A. Ruminahui, a gold-copper porphyry target on trend with Llurimagua (CODELCO) and Cascabel (Solgold)

- B. Los Osos, a gold-copper porphyry target close to the 17Moz Cangrejos deposit (Lumina Gold)

- C. Macara, a VMS target potentially with a gold oxide cap, and nearby porphyry potential

The Company is focused on advancing its 100%-owned projects and then seeking partnership with mid-tier or major mining companies contingent on initial exploration results.

Strategy: What is the Company planning to do?

The plan, as laid out in the corporate presentation and reiterated in news releases from 1 March 2019 through to 14 January 2020 inclusive, is to work up the prospects, drill the best targets on a 100% funded basis, manage existing treasury and then farm out. Salazar wants to repeat the project generator blueprint established at Curipamba by targeting the next 100%-owned discovery and trading the non-core assets.

As an aside, all exploration companies want to make a good discovery, and all exploration geologists want to intersect a hundred metres or more grading one gram of material or more. Exploration is one of the few industries where real capital value can be generated overnight with the drill bit. Adam Smith, David Ricardo and Karl Marx, the early political scientists established Land, Labour, Entrepreneurship, and Capital as the essential Factors of Production, and a mineral discovery will result in the Land value changing dramatically. As it happens, for a discovery to be made, an exploration company needs to harness the other three Factors of Production, work, wit, and finance. Salazar has a stated ‘aim of making Ecuador’s next significant copper-gold discovery’. The entrepreneurship, labour and capital is in hand and what the shareholders want to see is the use of these three Factors of Production applied to the fertile geology of Ecuador, in the licenses carefully selected by Fredy and his team.

Returning to Salazar Resources’s strategy, in January it announced that the Company “plans to drill Rumiñahui, Los Osos and Macara on a 100% basis in 2020 and evaluate strategic options as the projects advance. The Company also awaits the re-opening of the national mining register later this year with interest. Salazar Resources has four project applications pending, and it is hoped that at least one of these new projects will be awarded when the register reopens. In addition the Company will submit several further applications for new projects and concession areas when the mining register opens.”

The Company then goes on to state that it, “intends to open formal discussion for farm-outs later in the year”. In parallel, work continues on the portfolio that has already been farmed out, where Salazar is fully carried by Adventus.

The graphic above is taken from the Salazar Resources website. The image shows the division between the self-funded projects (on the left-hand side)and the fully carried projects (on the right-hand side). Note that Salazar Resources references projects in Colombia, but little detail or information on these projects is given.

Capital Structure

Directors and management own approximately 30% of the issued shares, with Arlington Capital and associates in London, UK accountable for another 15-20% of the issued share capital.

Arlington Capital holds the warrants at C$0.12. Named institutional investors include US Global Investors, Merian Global Investors, Galileo Global Equity Advisors, Arlington Capital, and BlackRock Advisors. Salazar Resources listed in 2007 at C$2.00 per share, and current prices are C$0.16 per share.

Liquidity in Salazar Resources is poor, as can be seen from the wide spread (often 3-4c), the blocky share price chart, and the statistics which show average daily volumes of 26,000 shares per day.